|  |

L' ARGENT , le métal de l'Espoir...

Au cours de l’histoire l’or a été l’argent des rois. Cependant, à travers la plupart des récits historiques, il a existé un métal bien plus important pour le commun des mortels que l’or. Dans les temps anciens c’était uniquement l’argent qui pouvait procurer à un esclave le seul moyen d’acheter sa liberté, ce qui a valu à l’argent l’appellation « métal de l’Espoir »

A quel point cela a t-il changé de nos jours? De nos jours l’argent continue de donner de l’espoir à des personnes partout dans le monde. Par exemple la médecine moderne procure des dépistages précoces, en protégeant la santé et la vie de plusieurs millions de personnes et est bâti autour d’un métal irremplaçable, l’argent. Les rayons X et les électrocardiogrammes seraient impossibles sans l’argent. L’élément de l’argent lui-même est connu pour procurer des bénéfices médicaux directs au corps humain et de nos jours existe à différents degrés dans la plupart des médicaments.

Pour la population qui vivait dans l’Athènes antique, l’argent leur procurait même un autre forme d’espoir : l’espoir de leur propre survie. L’histoire commence en 490 av-JC quand l’armée d’athéniens a malencontreusement perdu contre la puissante armée Perse à la bataille du Marathon. Pour les perses Marathon était une humble défaite qu’ils n’oublieront pas. En 480 av-JC la menace de la colère perse a grandi comme une sombre et violente tempête sur les athéniens. Chaque jour naissaient de nouvelles rumeurs sur la menace grandissante perse.

En 483 av-Jc l’argent fût découvert à Laurion, à environ 25 km d’Athènes. Le dépôt s’est révélé être important et beaucoup de l’argent miné fût converti en pièces drachmes appelées « Hiboux d’Athènes ». Thémistocle, fils de Neocles était un maître stratégique. Avec la mine d’argent de Laurion est venu l’espoir d’une future et décisive victoire et la fin de la tyrannie perse.

Compte tenu de ce que la bataille serait gagnée ou perdue en mer, Thémistocle a utilisé les profits de la mine pour construire une flotte de 200 navires de guerre. Le raisonnement de Thémistocle était simple, l’armée perse pouvait uniquement triompher que si elle était efficacement assistée par des équipements et communications procurés par leur flotte. Il savait également que la mer Egée était une mer violente et Thémistocle devait simplement attendre le bon moment.

En 480 av-Jc, fondé par les mines d’argent de Laurion, la flotte athénienne parvint à l’impossible et mis à jamais en défaite l’ancienne armée navale perse. La bataille navale de Salamis a mis un terme à l’oppression et l’impérialisme perse.

L’argent – devint dès lors le métal de l’espoir...

(Philip Judge)

Au cours de l’histoire l’or a été l’argent des rois. Cependant, à travers la plupart des récits historiques, il a existé un métal bien plus important pour le commun des mortels que l’or. Dans les temps anciens c’était uniquement l’argent qui pouvait procurer à un esclave le seul moyen d’acheter sa liberté, ce qui a valu à l’argent l’appellation « métal de l’Espoir »

A quel point cela a t-il changé de nos jours? De nos jours l’argent continue de donner de l’espoir à des personnes partout dans le monde. Par exemple la médecine moderne procure des dépistages précoces, en protégeant la santé et la vie de plusieurs millions de personnes et est bâti autour d’un métal irremplaçable, l’argent. Les rayons X et les électrocardiogrammes seraient impossibles sans l’argent. L’élément de l’argent lui-même est connu pour procurer des bénéfices médicaux directs au corps humain et de nos jours existe à différents degrés dans la plupart des médicaments.

Pour la population qui vivait dans l’Athènes antique, l’argent leur procurait même un autre forme d’espoir : l’espoir de leur propre survie. L’histoire commence en 490 av-JC quand l’armée d’athéniens a malencontreusement perdu contre la puissante armée Perse à la bataille du Marathon. Pour les perses Marathon était une humble défaite qu’ils n’oublieront pas. En 480 av-JC la menace de la colère perse a grandi comme une sombre et violente tempête sur les athéniens. Chaque jour naissaient de nouvelles rumeurs sur la menace grandissante perse.

En 483 av-Jc l’argent fût découvert à Laurion, à environ 25 km d’Athènes. Le dépôt s’est révélé être important et beaucoup de l’argent miné fût converti en pièces drachmes appelées « Hiboux d’Athènes ». Thémistocle, fils de Neocles était un maître stratégique. Avec la mine d’argent de Laurion est venu l’espoir d’une future et décisive victoire et la fin de la tyrannie perse.

Compte tenu de ce que la bataille serait gagnée ou perdue en mer, Thémistocle a utilisé les profits de la mine pour construire une flotte de 200 navires de guerre. Le raisonnement de Thémistocle était simple, l’armée perse pouvait uniquement triompher que si elle était efficacement assistée par des équipements et communications procurés par leur flotte. Il savait également que la mer Egée était une mer violente et Thémistocle devait simplement attendre le bon moment.

En 480 av-Jc, fondé par les mines d’argent de Laurion, la flotte athénienne parvint à l’impossible et mis à jamais en défaite l’ancienne armée navale perse. La bataille navale de Salamis a mis un terme à l’oppression et l’impérialisme perse.

L’argent – devint dès lors le métal de l’espoir...

(Philip Judge)

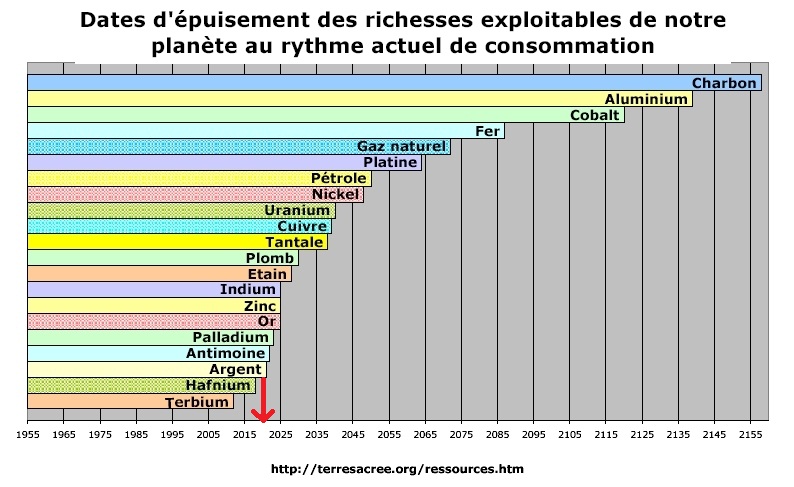

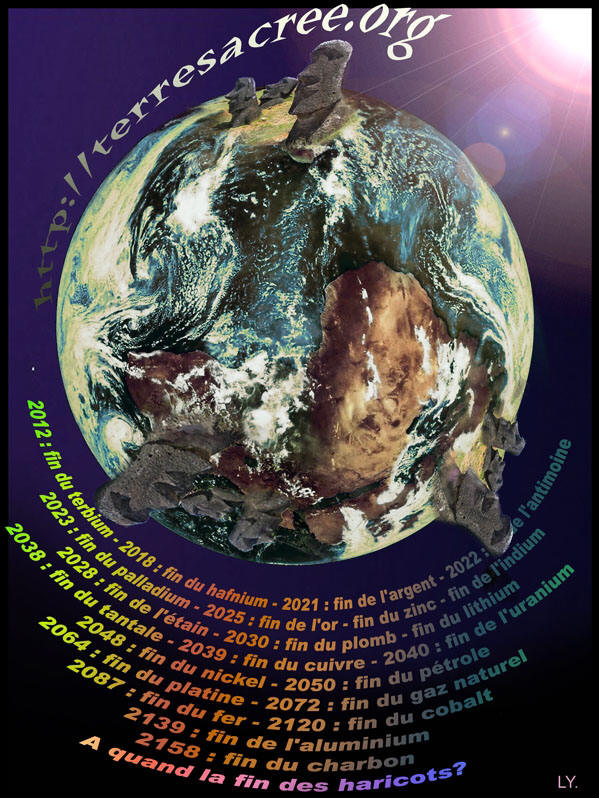

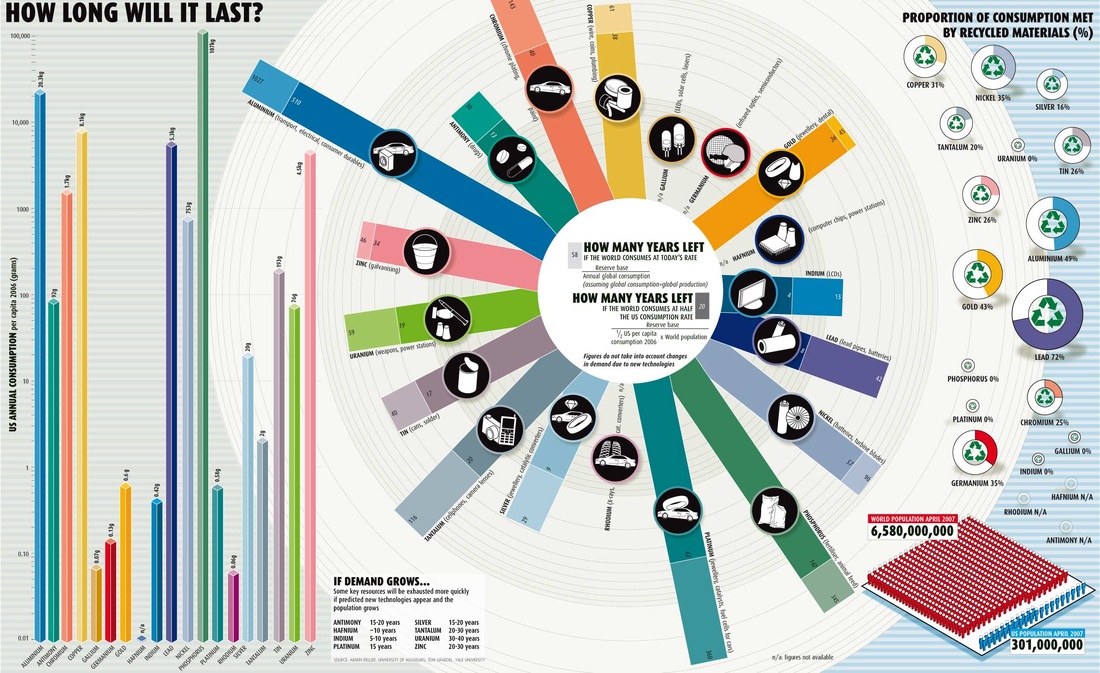

Un terrible échéancier

2012 : fin du terbium

2018 : fin du hafnium

2021 : fin de l' Argent métal

2022 : fin de l'antimoine

2023 : fin du palladium

2025 : fin de l' Or

fin du zinc

fin de l'indium2028 : fin de l'étain

2030 : fin du plomb

fin du lithium

2038 : fin du tantale

2039 : fin du cuivre

2040 : fin de l'uranium

...

2012 : fin du terbium

2018 : fin du hafnium

2021 : fin de l' Argent métal

2022 : fin de l'antimoine

2023 : fin du palladium

2025 : fin de l' Or

fin du zinc

fin de l'indium2028 : fin de l'étain

2030 : fin du plomb

fin du lithium

2038 : fin du tantale

2039 : fin du cuivre

2040 : fin de l'uranium

...

James Turk Reveals His Remarkable Response To The LBMA

Following up on Part I of his incredible interview regarding the truth about what is happening in the gold and silver markets as well as the FCA investigation into the gold market, today James Turk takes KWN readers around the world on Part II of a trip down the rabbit hole of bullion bank and government schemes.

Turk continues in part II of his KWN interview: Over the past two weeks the LBMA has been conducting a survey of market participants that trade physical silver. They are taking this step in response to the decision to end the daily silver fix.

The LBMA said: “In view of the recent announcement by the London Silver Market Fixing Ltd., it is important to gather the views of the global market to find a solution that meets the needs of market users around the world. The launch of the survey is an integral part of this process.”....

“The LBMA reported that more than 250 people responded to its survey, which ended Friday. Here is my response to the key questions the LBMA posed....

“1. Is the current silver price discovery method sufficient?

The market for silver derivatives dominates price discovery for physical silver, which explains why gold and silver have been in backwardation more often than not since July 2013. This backwardation is proof positive of the abnormal influence of silver derivatives on the pricing structure, as is the fact that commitments to deliver silver in the aggregate far exceed the annual new supply; they even exceed available above-ground supplies. In this regard, an analysis of U.S. Commodity Futures Trading Commission data shows that futures derivatives of commodities such as corn or soybeans do not exceed annual supply. Backwardation in gold in theory is impossible because it would mean participants are passing up the free arbitrage. Given that silver is a gold substitute in that at present 66 ounces of silver provide the same safe-haven characteristics as one ounce of gold (that is, money outside the banking system), backwardation in silver is impossible too, yet backwardation has prevailed on and off for months. That the LBMA 18 months ago stopped reporting SIFO shows how artificial the price curve is for silver. Back then the LBMA stated in effect that customers were unable to transact at the SIFO rate being quoted, which meant that paper pricing was unrealistic because sellers of paper were unable to commit to physical delivery at the prices being posted (that is, posted but not true dealing quotes). If silver derivatives did not dominate the pricing structure, the price of physical silver would be much higher. A similar situation prevails in gold, but is not as extreme (that is, prices in gold are not as unrealistically low as they are in silver).

2. What new improvements would you like to see/recommend?

There are two very different silver markets. One is for physical silver, which is a tangible asset of limited availability. The other one is for paper silver, which includes derivatives of all sorts that can be issued in essentially unlimited supply, meaning that it is impossible for ALL sellers of these derivatives to meet their commitments to deliver physical silver if called on to do so. The paper silver market is in effect a fractional reserve system, which obviously could result in adverse systemic consequences for banks and other participants should a silver squeeze occur (as it did in September 1979 to January 1980). These two silver markets need to be clearly delineated for the benefit of market participants, and the short side of the paper silver market needs to be controlled with rigid governors to impose discipline on the quantity of paper issued. If the prices of silver along the curve (that is, spot or forward) in these two different markets are to intersect as they do now, the shorts in the paper market need to prove that they can deliver physical metal. Doing so would improve the accuracy of any price discovery in the silver market by making spot and forward prices more realistic because they would become an authentic reflection of true supply conditions. Namely, there would be an acknowledgement that the supply of physical silver is limited. Thus, silver price discovery would be improved by imposing discipline that would prevent the paper shorts from dominating the price of physical silver.

3. What are the essential features that you would wish to see in any replacement?

Derivative contracts can settle in either cash or metal. Both the buyer and the seller need to put up margin as evidence of their ability to fulfill the terms of the contact they enter into. These margin requirements are now met generally by providing cash. Though margins can also be met with physical metal in some cases, it is rare. My proposal would be for cash settlement contracts to be margined with cash, regardless whether the participant is long or short the contract, and can be essentially unlimited in terms of the number of contracts issued. In contrast, derivatives that commit to deliver physical metal should be margined differently, in effect controlling the shorts which in turn also would result in disciplined control of the longs of these contracts. Those who have bought a contract that could result in the delivery of physical silver should meet their margin requirement with cash. But those who have sold short a contract that could result in the delivery of physical silver should meet their margin requirement by having physical metal stored in an LBMA-approved vault. As is now the case, the size of the margin requirement can be periodically set by an exchange for exchange-traded derivatives or a regulatory body such as the Bank of England for over-the-counter trade derivatives. Note that even though the short sellers of contracts that could result in the physical delivery of metal are meeting their margin requirement with physical metal, the fractional-reserve nature of the physical market will not disappear. For example, if a 50-percent margin requirement was imposed, the commitments to deliver physical metal in the aggregate could grow to twice the available stock, unless of course the short sellers have additional physical metal available that is not being put into LBMA vaults for margin. But the objective of requiring these short sellers to meet margin requirements with physical metal is not to try eliminating the fractional-reserve aspect of the market, which is probably an impossible task given the human tendency to expand credit. Rather it is simply a method of imposing prudent discipline on the silver market by controlling short sellers of silver derivatives.

4. Which market participants would be the ideal contributors to the pricing mechanism? (for example, bullion banks, manufacturers, refiners, others?).

All market participants should be the contributors to the pricing mechanism. When a trade takes place on an exchange or over the counter, the data of that trade should be immediately provided to neutral third parties to collect and report (for example, Bloomberg, Reuters, et al.). Aggregate data should also be reported. For example, this would include measurements of the total outstanding commitments for physical metal by size and forward date.

5. Other comments on the pricing mechanism?

While I have focused almost exclusively on silver, my analysis and recommendations also apply to gold.”

What all of this means, Eric, is that there is a practical way to eliminate the manipulation of gold and silver prices. It is to require that anyone selling short any derivatives contract that provides for the delivery of physical metal must meet margin requirements by having physical silver in a vault, and further that the margin requirement be reasonably high to control the fractional-reserve leveraging.

This step would prevent price manipulations like the one where Barclays Bank was caught and fined. Traders, whether acting for their bank’s account or as agents for government central planners, would no longer be able to conjure up out of thin air London good delivery bars in an attempt to force gold and silver prices lower by making believe that they have physical gold available for sale when in fact they don’t. A reasonably high margin requirement in terms of physical metal imposed on short sellers of physical metal would move price discovery in gold and silver back to where it should be based, which is the market for physical metal and not the derivatives market.

My recommendation is that a 50-percent margin requirement be imposed on short sellers of contracts of physical metal. So if someone sells short a contract obligating the delivery of physical metal, the short-seller needs to prove that he has at least 1 ounce of silver in a vault for every 2 ounces sold short.

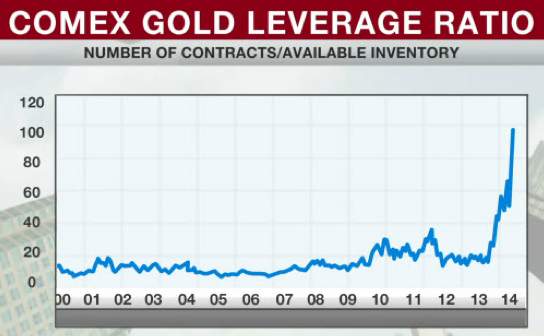

This measure will reduce the fractional-reserve aspect of precious metal trading to a reasonable level from the 100-to-1 level, which some market participants have stated is the present ratio of paper commitments to actual physical metal available. Not only will reasonable margin requirements reduce the opportunity to manipulate gold and silver prices with derivatives, it will also offer the added benefit of lowering the possibility of systemic risk like what occurred in 2008.

Now here’s the important point. Fractional-reserve systems are not only fraudulent because of the inability to deliver all commitments; they are also inherently unstable and come with incalculable risks. For this reason I therefore always recommend avoiding paper products, and owning only physical gold and physical silver. When you own physical metal, you are going to be safe when the next 2008-like systemic collapse arrives.”

IMPORTANT - To read Part I of Turk’s incredible interview CLICK HERE.

Following up on Part I of his incredible interview regarding the truth about what is happening in the gold and silver markets as well as the FCA investigation into the gold market, today James Turk takes KWN readers around the world on Part II of a trip down the rabbit hole of bullion bank and government schemes.

Turk continues in part II of his KWN interview: Over the past two weeks the LBMA has been conducting a survey of market participants that trade physical silver. They are taking this step in response to the decision to end the daily silver fix.

The LBMA said: “In view of the recent announcement by the London Silver Market Fixing Ltd., it is important to gather the views of the global market to find a solution that meets the needs of market users around the world. The launch of the survey is an integral part of this process.”....

“The LBMA reported that more than 250 people responded to its survey, which ended Friday. Here is my response to the key questions the LBMA posed....

“1. Is the current silver price discovery method sufficient?

The market for silver derivatives dominates price discovery for physical silver, which explains why gold and silver have been in backwardation more often than not since July 2013. This backwardation is proof positive of the abnormal influence of silver derivatives on the pricing structure, as is the fact that commitments to deliver silver in the aggregate far exceed the annual new supply; they even exceed available above-ground supplies. In this regard, an analysis of U.S. Commodity Futures Trading Commission data shows that futures derivatives of commodities such as corn or soybeans do not exceed annual supply. Backwardation in gold in theory is impossible because it would mean participants are passing up the free arbitrage. Given that silver is a gold substitute in that at present 66 ounces of silver provide the same safe-haven characteristics as one ounce of gold (that is, money outside the banking system), backwardation in silver is impossible too, yet backwardation has prevailed on and off for months. That the LBMA 18 months ago stopped reporting SIFO shows how artificial the price curve is for silver. Back then the LBMA stated in effect that customers were unable to transact at the SIFO rate being quoted, which meant that paper pricing was unrealistic because sellers of paper were unable to commit to physical delivery at the prices being posted (that is, posted but not true dealing quotes). If silver derivatives did not dominate the pricing structure, the price of physical silver would be much higher. A similar situation prevails in gold, but is not as extreme (that is, prices in gold are not as unrealistically low as they are in silver).

2. What new improvements would you like to see/recommend?

There are two very different silver markets. One is for physical silver, which is a tangible asset of limited availability. The other one is for paper silver, which includes derivatives of all sorts that can be issued in essentially unlimited supply, meaning that it is impossible for ALL sellers of these derivatives to meet their commitments to deliver physical silver if called on to do so. The paper silver market is in effect a fractional reserve system, which obviously could result in adverse systemic consequences for banks and other participants should a silver squeeze occur (as it did in September 1979 to January 1980). These two silver markets need to be clearly delineated for the benefit of market participants, and the short side of the paper silver market needs to be controlled with rigid governors to impose discipline on the quantity of paper issued. If the prices of silver along the curve (that is, spot or forward) in these two different markets are to intersect as they do now, the shorts in the paper market need to prove that they can deliver physical metal. Doing so would improve the accuracy of any price discovery in the silver market by making spot and forward prices more realistic because they would become an authentic reflection of true supply conditions. Namely, there would be an acknowledgement that the supply of physical silver is limited. Thus, silver price discovery would be improved by imposing discipline that would prevent the paper shorts from dominating the price of physical silver.

3. What are the essential features that you would wish to see in any replacement?

Derivative contracts can settle in either cash or metal. Both the buyer and the seller need to put up margin as evidence of their ability to fulfill the terms of the contact they enter into. These margin requirements are now met generally by providing cash. Though margins can also be met with physical metal in some cases, it is rare. My proposal would be for cash settlement contracts to be margined with cash, regardless whether the participant is long or short the contract, and can be essentially unlimited in terms of the number of contracts issued. In contrast, derivatives that commit to deliver physical metal should be margined differently, in effect controlling the shorts which in turn also would result in disciplined control of the longs of these contracts. Those who have bought a contract that could result in the delivery of physical silver should meet their margin requirement with cash. But those who have sold short a contract that could result in the delivery of physical silver should meet their margin requirement by having physical metal stored in an LBMA-approved vault. As is now the case, the size of the margin requirement can be periodically set by an exchange for exchange-traded derivatives or a regulatory body such as the Bank of England for over-the-counter trade derivatives. Note that even though the short sellers of contracts that could result in the physical delivery of metal are meeting their margin requirement with physical metal, the fractional-reserve nature of the physical market will not disappear. For example, if a 50-percent margin requirement was imposed, the commitments to deliver physical metal in the aggregate could grow to twice the available stock, unless of course the short sellers have additional physical metal available that is not being put into LBMA vaults for margin. But the objective of requiring these short sellers to meet margin requirements with physical metal is not to try eliminating the fractional-reserve aspect of the market, which is probably an impossible task given the human tendency to expand credit. Rather it is simply a method of imposing prudent discipline on the silver market by controlling short sellers of silver derivatives.

4. Which market participants would be the ideal contributors to the pricing mechanism? (for example, bullion banks, manufacturers, refiners, others?).

All market participants should be the contributors to the pricing mechanism. When a trade takes place on an exchange or over the counter, the data of that trade should be immediately provided to neutral third parties to collect and report (for example, Bloomberg, Reuters, et al.). Aggregate data should also be reported. For example, this would include measurements of the total outstanding commitments for physical metal by size and forward date.

5. Other comments on the pricing mechanism?

While I have focused almost exclusively on silver, my analysis and recommendations also apply to gold.”

What all of this means, Eric, is that there is a practical way to eliminate the manipulation of gold and silver prices. It is to require that anyone selling short any derivatives contract that provides for the delivery of physical metal must meet margin requirements by having physical silver in a vault, and further that the margin requirement be reasonably high to control the fractional-reserve leveraging.

This step would prevent price manipulations like the one where Barclays Bank was caught and fined. Traders, whether acting for their bank’s account or as agents for government central planners, would no longer be able to conjure up out of thin air London good delivery bars in an attempt to force gold and silver prices lower by making believe that they have physical gold available for sale when in fact they don’t. A reasonably high margin requirement in terms of physical metal imposed on short sellers of physical metal would move price discovery in gold and silver back to where it should be based, which is the market for physical metal and not the derivatives market.

My recommendation is that a 50-percent margin requirement be imposed on short sellers of contracts of physical metal. So if someone sells short a contract obligating the delivery of physical metal, the short-seller needs to prove that he has at least 1 ounce of silver in a vault for every 2 ounces sold short.

This measure will reduce the fractional-reserve aspect of precious metal trading to a reasonable level from the 100-to-1 level, which some market participants have stated is the present ratio of paper commitments to actual physical metal available. Not only will reasonable margin requirements reduce the opportunity to manipulate gold and silver prices with derivatives, it will also offer the added benefit of lowering the possibility of systemic risk like what occurred in 2008.

Now here’s the important point. Fractional-reserve systems are not only fraudulent because of the inability to deliver all commitments; they are also inherently unstable and come with incalculable risks. For this reason I therefore always recommend avoiding paper products, and owning only physical gold and physical silver. When you own physical metal, you are going to be safe when the next 2008-like systemic collapse arrives.”

IMPORTANT - To read Part I of Turk’s incredible interview CLICK HERE.

RSS Feed

RSS Feed